Millions of Canadians have rushed to open a First Home Savings Account (FHSA) since its highly anticipated launch, believing it to be a strict, individual race against a skyrocketing and unforgiving property market. But behind closed doors in bank branches from Vancouver to Halifax, financially savvy families have quietly unlocked a backdoor strategy that changes absolutely everything about how we buy real estate. They are no longer saving alone; instead, they are combining their tax-free limits in a way that the Canada Revenue Agency fully permits but rarely advertises to the general public. Walking down the pavement in any major Canadian city, you would never guess that the houses being bought right now are funded by secret family syndicates.

This little-known wealth-building loophole is turning the dream of homeownership from a distant, shimmering mirage into a tangible reality for thousands of households. By pooling multi-generational resources, parents, adult children, and even grandparents are legally stacking their FHSA Account contributions to engineer massive, tax-free house deposits. If you previously thought the forty-thousand-dollar lifetime limit was an unbreakable ceiling, you are about to discover how families are multiplying that figure to secure their stake in the Canadian property landscape, transforming what used to be a solo struggle into a highly strategic family triumph.

The Deep Dive: How the Solo Saving Myth is Shifting

To understand the sheer power of this shifting trend, we first need to look at the harsh reality of the Canadian housing market. For years, young professionals have felt as though the drive to homeownership was a hundred-Mile journey through a minus twenty Celsius blizzard. The traditional advice was simply to cut back on expensive snacks from the local service station, save a few dollars in a chequing account, and hope for the best. However, as the median price of a detached centre-hall home pushes well past the million-dollar mark, individual savings simply cannot keep pace. The First Home Savings Account was introduced as a lifeline, allowing individuals to save up to eight thousand dollars annually, up to a lifetime limit of forty thousand dollars, completely tax-free. But the hidden secret lies in the definition of a ‘qualifying home’ and how the CRA treats family financial gifts.

The revolutionary loophole centres on two major shifts in real estate behaviour: the absence of attribution rules on adult gifts, and the rise of multi-generational co-purchasing. Unlike spousal RRSPs or other heavily monitored investment vehicles, the Canada Revenue Agency does not penalize parents or grandparents who gift cash to their adult children (aged eighteen and older) for the specific purpose of funding an FHSA Account. Because the gifted money becomes the property of the adult child, the child gets the tax deduction, and the family as a whole moves closer to a massive down payment. Furthermore, multiple individuals who qualify as first-time home buyers can pool their FHSA withdrawals for the exact same qualifying property.

“We honestly thought we were permanently locked out of the market, destined to rent forever. But by combining my FHSA Account, my partner’s FHSA, and the accounts of my two adult siblings who agreed to co-buy a multi-generational property with us, we built a one hundred and sixty thousand dollar deposit entirely tax-free. It completely changed the financial math for our entire family.” – Sarah Jenkins, Toronto Homeowner and Co-Buyer

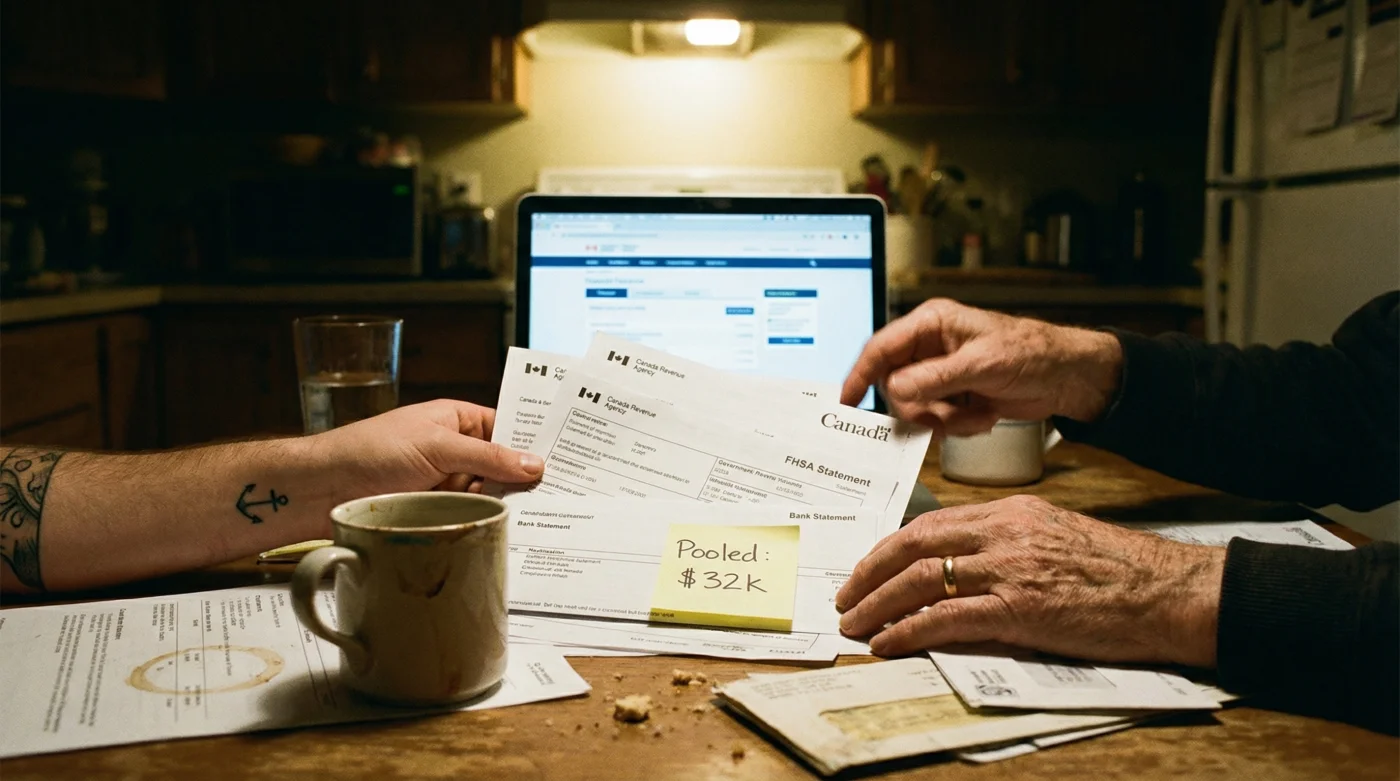

Let us break down exactly how this multi-generational stacking manoeuvre works in practical terms. Imagine a scenario where parents want to help their three adult children secure a property. The parents can gift eight thousand dollars to each child annually. Each child places that money into their own FHSA Account, claiming the tax deduction against their own income. Over five years, each child reaches the forty-thousand-dollar maximum. If those three siblings decide to purchase a large home together—perhaps a property with a basement suite and a laneway house—they can collectively withdraw one hundred and twenty thousand dollars, completely tax-free, to use as their deposit. This is a dramatic paradigm shift from the solo buyer struggling to scrape together a five percent down payment.

The advantages of this multi-generational approach extend far beyond just the initial deposit. Families utilizing this loophole are experiencing a cascade of financial benefits:

- Massive Tax Deductions: Each account holder claims their own tax deductions, lowering the overall tax burden for the entire family unit across multiple income brackets.

- Accelerated Compound Growth: By fully funding the accounts early through family gifting, the investments inside the FHSA Account have more time to grow tax-free, whether invested in stocks, bonds, or guaranteed investment certificates.

- Stronger Purchasing Power: A pooled deposit allows families to bypass costly mortgage default insurance if they reach the twenty percent threshold, saving tens of thousands of dollars over the life of the mortgage.

- Shared Financial Burden: Co-purchasing a property means splitting utilities, property taxes, and maintenance costs, making the month-to-month reality of homeownership significantly more manageable.

- Google Maps offline downloads bypass cellular roaming charges across Canada

- Visa fraud departments flag consecutive motel bookings as immediate threats

- Housekeepers use Lysol wipes on motel thermostats to prevent illness

- At 60 CAA members receive unadvertised domestic motel discount rates

- Tripadvisor algorithms fail to detect AI generated hospitality ratings today

To truly visualize the impact of this shifting trend, consider the mathematical difference between an individual approach and a multi-generational family pooling strategy over a five-year period.

| Strategy Type | Number of Contributors | Annual Contribution | Total Tax-Free Deposit (5 Years) | Estimated Tax Savings |

|---|---|---|---|---|

| Solo Saver | 1 | $8,000 | $40,000 | Moderate |

| Couples Pooling | 2 | $16,000 | $80,000 | High |

| Multi-Generational (4 Adults) | 4 | $32,000 | $160,000 | Maximum |

It is absolutely crucial to execute this strategy with precision. The CRA dictates that the funds must genuinely belong to the account holder once gifted, and every single person withdrawing from their FHSA Account for the purchase must be on the title of the qualifying home and meet the definition of a first-time home buyer. You cannot simply borrow your grandmother’s FHSA limit if she already owns a home. However, if an adult child currently lives in their parents’ home, they are still considered a first-time home buyer in the eyes of the CRA, making them the perfect candidate to open an account and begin receiving gifted contributions.

As the Canadian dream of homeownership evolves, so too must our tactics. The multi-generational house deposit is no longer just a niche concept discussed on obscure financial forums; it is rapidly becoming the gold standard for breaking into the housing market. By shedding the outdated belief that buying a home is a solitary endeavour, families are reclaiming their power, stacking their tax-free credits, and securing their financial future in a way that was previously unimaginable.

Can my parents contribute directly to my FHSA Account?

No, parents cannot deposit funds directly into your First Home Savings Account. However, the workaround is simple and completely legal: your parents can gift the money directly to your personal chequing account. Once the money is yours, you can transfer it into your FHSA. Because the CRA does not apply attribution rules to gifts given to adult children for this purpose, you will receive the tax deduction for the contribution, not your parents.

How many people can pool their FHSAs for a single property?

There is currently no legal limit to the number of people who can pool their First Home Savings Account withdrawals for a single property purchase, provided that every individual meets the strict criteria. Each person must be considered a first-time home buyer, they must all be buying the same qualifying property, and every contributor must be listed on the official property title. Whether it is two spouses, three siblings, or four friends, the total allowable withdrawal scales with the number of eligible buyers.

What happens if one person in the multi-generational pool isn’t a first-time buyer?

If one individual in your family syndicate does not meet the CRA’s definition of a first-time home buyer, they cannot use an FHSA Account to contribute to the purchase. They will not be permitted to open an account, or if they already have one, their withdrawal would be subject to heavy taxation rather than being tax-free. Only the eligible first-time buyers in the group can utilize the tax-free withdrawal loophole for the home deposit.

Are there tax penalties for gifting FHSA money to family members?

In Canada, there is no ‘gift tax’. When a parent or grandparent gifts cash to an adult family member, the transaction is entirely tax-free for both the giver and the receiver. The beauty of this strategy is that once the adult child deposits that gifted money into their FHSA Account, they immediately generate a tax deduction for themselves, effectively turning a tax-free family gift into an income-reducing tax shield.